Uber Mumbai has just announced a big hike on the Black and SUV services, pretty much bringing them on par with the Ola Prime SUV service. So here’s the latest fare chart (older versions here – v1, v2):

Approx. taxi fares in Mumbai as on 13 July 2015

Note on the calculation methodology:

Travel time calculated assuming 3 min per km (Uber, Ola, TFS)

Waiting time taken as 1/2 min per km (kaali peeli & Meru\TabCab)

I’ve been using Uber quite frequently over the last couple of months and today’s Mumbai taxi strike to protest such services ironically forced me to opt for Uber at a 1.8x surge price. While I’ve had my share of ups & downs with Uber, the flexible pricing model has been one aspect that I’ve been impressed with compared to the competition like Ola.

Uber managed to create quite a buzz offering single digit per km rates which was almost half the rate others were offering at that time, but the pricing model which included a per minute charge on the trip ensured that the overall fare was not unsustainably low. This has also allowed them to go after the local taxi & auto services in the different cities and they also end up being cheaper for medium to long distances.

The Uber pricing in India is typically a low per km rate coupled with another per trip minute rate on top of a fixed base fare, with the overall fare subject to a minimum amount and of course the surge factor. Putting it simply:

Fare = Surge factor x (Distance x Rate per km + Trip time in minutes x Rate per minute)

Ola which had started off in India with a conventional pricing model of rate per km and a waiting time rate has pretty much overhauled their pricing to mimic the Uber model. They have in fact abandoned their initial method of applying a fixed peak time price during 2 slots on weekdays in favour of a surge factor. The other taxi services like Meru, Tab Cab, Easy Cab etc. have thus far stuck to the traditional model, though they’re trying to stay relevant through special offers.

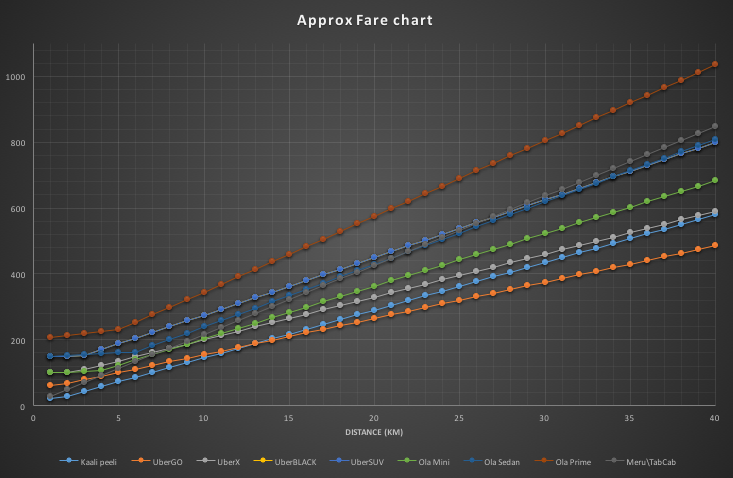

I also did a simplistic analysis of how the different services compare in terms of the trip fare in a city like Mumbai (Google Sheet here). I’ve assumed a trip time of 3 minutes per km and waiting time of 1 minute for every 4 km, so the results are going to be quite different in heavy traffic.

Approx fare comparison (corrected)

For short distances, the local kaali peelis are of course the cheapest, but for distances above 10 km, UberGO ends up being a better deal. The next cheapest is the Ola mini which starts getting pretty competitive with kaali peelis after the 20 km mark. This is of course disregarding the non-AC nature of the kaali peelis. [Update] Ola Mini and UberX are pretty competitive till the 10 km range, but separate pretty quickly after that as the near 30% higher charge per km for Ola starts making a mark.

The older generation of Meru, Tab Cab etc manage to remain competitive with the newer lot, matching the next best Ola Sedan UberX and Ola up to the 10 km mark, but the higher cost per km quickly multiplies beyond that point. And then we have UberBLACK and UberSUV which have the same rates but different capacities. They can actually offer a better deal than Meru and the likes for long distances over 25 km. Of course if you have 5-6 people travelling, then these 6 seaters are the way to go. Lastly, we have Ola’s version of the SUV with its Prime service that’s the costliest of the lot. Again, if you are in a group of 5-6 people, this can actually be cheaper than the taking two 4-seater vehicles, unless of course you manage to get a couple of UberGOs.

I haven’t considered the surge pricing in the above comparison, and that is a scenario where the older lot turns out to be cheaper. However, such scenarios are rare as Merus and the likes can be pretty hard to find for immediate travel. The interesting thing to see now will be the role that regulators play in toying around with these pricing models.

Update (16 Jun 2015): Found a major miscalculation in the trip time. I have corrected the graph and updated the text accordingly.

Now that Apple has announced that OS X updates will be free going forward, and many of its first party apps like iWork are going to be free with new devices, Microsoft seems to have its task cut out. Many people seem to think that this move by Apple will really hurt Microsoft. In some ways Apple is trying to commoditize software the way Microsoft commoditized hardware over the last 2 decades. However, there are a few key points that not many have mentioned:

Microsoft has given away major OS updates for free. E.g. Windows XP SP2. In a way, the Apple move was preempted by the free Windows 8.1 update.

Microsoft is a past master of bundling free software with its OS. Remember Internet Explorer vs Netscape? Or more recently, Office being given away with Windows RT.

Apple hardware remains luxury items, and free OS upgrades are not going to make budget conscious people switch from Windows to Apple devices. That said, the real threat comes when people realize that a tablet meets their requirements and is probably cheaper than a PC (desktop\laptop) when it is time to get a new device.

The real threat to Microsoft comes from Android, as OEMs are gradually warming up to Android as an alternative for Windows for laptops. Since the market is undergoing a major shift in the kind of personal devices being used (desktops to laptops to mobiles & tablets), there is a big scope for a free OS. Android has been successful on mobiles while Linux failed on PCs due to this very reason.

OS development has an associated cost even if you do not pay a third party for it. Apple is just subsidizing the software costs through hardware margins. Even if OEMs decide to opt for Android or Chrome OS, they will need an in house team to customize the OS. Of course, OEMs probably already have an in house team developing software for Windows given the typical bloatware that comes pre-installed on PCs.

The bottom line is that Microsoft has to continue to woo its OEM partners who bring in the OS revenue, while at the same time transform its revenue source to hardware. The Nokia acquisition becomes even more important now.

After my post on diamonds and water, I came across a really detailed article – The Price of Wine – on how the price and brand of wine influences the “taste-buds”. Also covers the wine investment market and wine making. This bit sums up the taste bit:

However, it’s unclear whether anyone can tell the difference between a $2,000 Lafite Bordeaux and a $3 table wine. In fact, most wine economists consider the matter settled. Blind tastings and academic studies robustly show that neither amateur consumers nor expert judges can consistently differentiate between fine wines and cheap wines, nor identify the flavors within them.

Given that most people think that the Post-PC era is on, it makes sense for Apple to continue its Mac pricing. The tablets and smartphones are anyway eating into the low end of the PC market:

The conventional wisdom is to pursue profits by maximizing market share. Apple pursues profits by specifically targeting only the high-margin segments of the overall market, and effectively forgoing market share in the low-margin segments, no matter how large those low-margin segments are.